AI's Impact on Accounting Industry

Introduction

Artificial Intelligence (AI) has been the foundation on which the extension of computing capabilities of current accounting systems has been managed progressively by increasing numbers of financial institutions. The infusion of the AI within the accounting operational field has been an unrelenting expansion of the functionalities of such a technical novelty in the disciplines of accounting. The rationale behind such expansion of AI is indicative of upgrading of a host of different functionalities of the accounting industry. These functionalities could be recognised as business efficiency, reduction of errors, controlling and prevention of organisational risks, competitiveness improvement and to formulate predictive operational arrangements. AI does enable the computing systems to make accurate predictions as well as institute changes in an according manner. This contributes to improve the accuracy of the automated work management systems in accounting through machine based learning. Thus, based on this concept of Artificial Intelligence applications within the accounting industry, the corresponding research proposal would be discussing the impact of AI on the accounting industry. The empirical research would be concentrating upon the exploration of the relative impact of AI on the diversified roles executed by the accounting professionals in their responsibility scenarios. The research proposal would be formulated to measure the impact of AI on the productivity improvement functionalities of the accounting professionals. The research proposal would be highlighting the research background and the selected rationale of the research proposal regarding the impact of AI on the management of the accounting standards by the professionals under consideration. Furthermore, the research aims and objectives would be formulated to determine the future research orientations. This would effectively clarify the purpose of the research questions and objectives.

The research literature review section would be formulated to evaluate the previously available research material regarding the topic under consideration so as to generate a critical review of the accessible information concerning the basic research questions. The parameters of the research questions and objectives would be put into effect to search for, evaluate and relate the findings to the research questions and objectives. Finally, the research methodology section in the Part III of the research proposal would be utilised to explain, discuss and justify the selection of particular research methods such as the research designs, research philosophy and the research approach. The data collection method and the relevance of the same would be highlighted as well. The process of establishment of clarity of the findings through the collection process would be determined as well. Finally, the research proposal would culminate through the outlining of the identified research limitations and ethical considerations which would be invested in the future research project which would be formulated on the basis of the corresponding proposal.

Research Background

According to Luo, Meng and Cai (2018), over the previous decades, the trend of increasing automation has been embraced by the accountants for the purpose of improvement of effectiveness and productivity in the accounting functioning.Kokina and Davenport (2017)have opined that, within the accounting profession, rote task responsibilities are executed by the professionals. Such responsibilities are oriented towards previewing, annotating, summarising, comparing and contrasting of the data and information inputs related to the repetitive tasks. In this context, the applications of AI are meant to improve the investment of human capabilities to a greater extent. The increasing complications related to the automated tools of AI based applications have been the source of considerable shortcomings in the appropriate technical toolsutilisation by the accounting professionals for the purpose of accounting tasks management. In contrast to this, the latest generation of AI systems have begun to explore the significance of human decisions and expertise as well as the limitations of digital automated machinery. Such processes have been consistently contributing to the advent of AI based functionality management approaches within the accounting industry(Mirzaey, Jamshidi and Hojatpour, 2017). According to Skilton and Hovsepian (2017), the development of AI could be conceptualised to be the prime factor in the influence of digitised working functionalities which are integral concerning the Fourth Industrial Revolution. The concept of the 4th Industrial Revolution has been established on the global availability of the digital technologies which had been spawned by the Third Industrial Revolution (based on the digital and IT expansion). Bloem et al (2014) have stated that convergence of biological, physical and digital innovations would be formulating the basis for the 4th Industrial Revolution. Schwab (2017) has further explained that in a similar manner to the advent of steam power of the 1st Industrial Revolution, the mechanised mass manufacturing and production of the 2nd Industrial Revolution and Digitisation of the 3rd Industrial Revolution, the 4th Industrial Revolution would be constituted in the major part by emerging technologies such as Artificial Intelligence (AI), Augmented Reality (AU), Genome Editing, Robotics and 3-D printing. In this context, the application of AI in the accounting sector and the subsequent impact on the accounting professionals would be reflective of the rapid changes in the manner in which creation, exchanges and distribution of the value of functioning could be performed at the industrial levels.

Furthermore, the background of the study could be better delineated through the observations of Omoteso (2012)as the conscious replication of human intelligence at the diversified workplaces, including within the accounting industry. It encompasses much more than the management of simplified digital entry of information and statistical data within computerised data bases. Primarily, the background of this research proposal has thus been determined as the study of the emergence of a synergistic accounting system by combining automation of rote tasks, advanced accounting software and the AI based operational mechanism. The study would be thus cognisant about detection of the productive activity improvement which could be achieved through combining the AI applications with existing accounting software systems to expand the efficacy of accounting operations in the current contextual scenario (Tredinnick, 2017).

Research Rationale

The rationale of the research is oriented towards discussing the empirical evidence which could be gathered concerning the impact of AI on various operational aspects as these are performed by the accounting professionals of specific organisations. The focal points of the research process would be the particular points of concern regarding the influence of AI on supervision of operational processes, the impact on decision making since the capability scenario could change drastically within the accounting institutions and the possibility of a negative impact on the job prospects of the accounting professionals. In this context, Moudud-Ul-Huq (2014) has also observed that AI technology has been utilised increasingly by accounting institutions to perform various administrative tasks and this practice has led to some structural changes in the methods through which such industrial entities perform. One particular objective of the subsequent research proposal would be to determine the extent to which such structural changes have been instituted in the accounting industry through the application of AI based applications such as the Expert System.

Research Aim

The aim of the research is to explore the impacts of Artificial Intelligence on the functionalities of accounting professionals in the respective industries.

Research Objectives

To identify the various impacts of AI on the roles of the accounting personnel related to the accounting organisations.

To assess the extent of structural changes which have become prevalent within the accounting institutions involving the impacts of AI based functionalities.

To evaluate the effects of AI on the roles of the accounting personnel concerning such technological impacts on employment structure for such professionals.

To recommend suitable future research prospects through which greater empirical research could be performed in this context.

Research Questions

What are the impacts of AI on the roles of the accounting personnel related to the accounting organisations?

What is the extent of structural changes which have become prevalent within the accounting institutions involving the impacts of AI based functionalities?

What are the effects of AI on the work roles of the accounting personnel concerning such technological impacts on employment structure for accounting professionals?

What are the prospects through which greater empirical research could be performed in this context?

Research Context

To this effect, the focus of the research towards measuring the application of AI within the particular disciplines of the accounting industry is to evaluate the impact of the differing technological developments on the changing patterns of role and performance of the accounting professionals within the organisational settings of the accounting and financial institutions.Marshall and Lambert (2018) have specified that a number of researchers had already investigated the utilisation of Artificial Intelligence applications, such as the Expert Systems (ES), within the processes of accounting pertaining to the impact of AI on the role of accountants. However, as has been opined by Gordon (2018), previously conducted research had not been systematic in terms of examining the issues which are associated with the improvement of AI based problem solving and work supervision processes of accounting work. Apart from this, previously performed research had also mostly focused on the expected benefits which could be derived from the application of Artificial Intelligence based technology and the transformative impacts of such technology based work process progression on the roles of the accountants have not been defined clearly. Furthermore, Issa, Sun and Vasarhelyi (2016)have been off the opinion that Accounting Systems would be requiring greater incorporation of artificial intelligence based operations management procedures so as to reinforce the traditional roles of accountants in management and evaluation of data. The benefits would be greater accuracy management in the balance sheets, effective generation of precise reports and saving of time since manual input of data could be avoided completely.This would require the review of the traditional work roles of the accountants which are, nevertheless, slated to be transformed to varying extents, provided the particular nature of the work disciplines.

To this effect, the corresponding research proposal would be evaluating the differential impacts of the AI on the operational roles of the accountants at different institutions. The research would also emphasize on specifying out the potential of AI in enabling the accounting institutions to realise competitive advantage achievement opportunities.

Research Significance (potential contributions)

The significance of this research could be outlined from multiplicity of perspectives. The first is the prospect of upgrading of skills of the human resources through increased exposure to the AI applications. The second one is the comprehensive transformation of the accounting roles of such professionals with the ambits of the financial institutions. The third one could be the development of organisational functional strategies through which better management of increased workloads in the accounting management systems could be developed through inclusion of AI in the digital automated accounting management systems.In this context, the analysis of AI applications and impact on the roles and work process of accounting professionals require assessment from the perspective of general technical upgrades. However, the significance of such a technological process could be discerned as the paradigm shift in the automated work process management procedures related to the conventional roles of accounting professionals. This shift has been engendered by the inclusion of AI applications in the accounting processes to better facilitate the performance improvement perspectives pertaining to the accounting professionals.Thus, the core elements of AI technology could be considered to be the information and knowledge which could be obtained by the artificial intelligence systems to perform a broad range of accounting tasks. Such information and knowledge could only be obtained through sequential analysis and recording of differential operational processes through which various professional roles are executed by the accounting professionals.The factor of machine learning becomes critical in this perspective. However, since the types of data and information as well as their purpose could consistently vary within the different accounting standards and functionalities, the impacts of AI on professional roles of the accountants could as well vary to certain extents. Another significant aspect of the research could be comprehended in this context that the empirical evidence based research would be striving towards the exploration of different methods through which interpretation of such extensive and variegated data could be leveraged by a combination of artificial and human intelligence to analyse the changing involvement patterns of accounting professionals in their work roles in an effective and instantaneous manner.

Literature Review

Financial institutions are provided with multiplicity of opportunities regarding enhancement of operational efficacy through AI based work process utilisation and through aligning their primary task management mechanisms with the AI based tools such as the previously mentioned Expert Systems (ES). However, the opportunities which are integral to the AI, are indicative of the radical changes in decision formulation regarding the multi-tasking processes which the accounting professionals have to appropriately manage. In case of calculations required to be performed by the accountants, as have been researched byShi (2019), the particulars and specifics could be automatically detected by the AI applications. This process also extends to the determination of the types of invoices and the status of payment remission. Furthermore, AI effectively manages the responsibility profiles of accountants through precision formulation of the records and the development of systems through obtaining learning experience from the previously documented processes which the artificial intelligence based memory segments could have recorded.

Functionalities

According toLi and Zheng (2018), the automation of accounting operations management, in an augmentation to the existing human resources working for the global accounting industry, at the conceptual levels, commenced two decades earlier. Prior to such a development, the various solutions which had existed, were completely different from the current AI based approaches. Nowhere else was this greater apparent than in the reliability, accuracy, performance, credibility and time consumption reduction aspects. However, the earlier solutions had been also oriented towards obtainment of identical objectives. Brynjolfsson, Rock and Syverson (2017) have recognised such objectives, from the performance perspective of the accounts industry, to be the automation of tedious, repetitive and interminable tasks and the optimisation of the various financial calculation processes so that operational efficiency could be improved. Guo (2019)has outlined that prior to the advent of AI, accounting professionals had to formulate and process invoices, purchase and delivery orders manually. The financial statements had to be manually entered into the computerised computations systems for the purpose of encoding and final transmission to the managerial personnel of the respective accounting institutions for the obtainment of approval. However, the advent of artificial intelligence based operational procedures has completely abolished the necessity of manual approach based accounting operations. In this context, the accounting workflows, now, could operate automatically through the AI systems software which could analyse, recognise, direct and publish the data and the analytical outcomes within the enterprise resource and financial systems documents as well as in the annual financial statements of the respective accounting institutions. Prior to the automation of such processes through the adoption of AI, the timings and details of the payments were not possible to be either tracked or predicted accurately. However, for the accounting professionals, the gaining of complete access into the necessary information within real time has become possible.

AI assisted accounting functionality specifications

Currently, as has been outlined by Appelbaum et al (2017), the statistical accounting data recording, handling and processing tasks have become completely automated through AI. Thus, the key procedural change in this context, could be identified as, enforcement of compliance. Skilton and Hovsepian (2017)have elaborated on this through observing that such an impact of AI on the accounting professionals is facilitated through the fact that any data which could be now autonomously generated by the AI based accounting systems, would be having extensively assured levels of accuracy. Such accurate generation of reports could further be completed within the least period of time since manual inputs are not required. Furthermore, the procedural changes in accounting management and standardisation through the application of AI could be recognised as the considerable changes in categorisation and recognition of data which could be derived from diverging and opposing sources to the appropriate accounting head. Apart from these, AI based automated processes could also handle various tasks which usually had to be performed by dedicated and specialised accounting personnel previously. Such tasks generally are processing of account receivable and payables as well as the data regarding payments which could have been already remitted. Such changes have positively contributed to the cost management betterment of the accounting firms.

Factors of AI

According to Pannu (2015), the trend of industrial application of AI systems in the accounting services has been premised upon the factors of maturity and reliability of such systems in terms of the efficacy which could be derived from application of these into differential accounting tasks. This reliability factor is defined through the reliability and flexibility of algorithms which govern the core functionalities of AI in the accounting sectors (Moudud-Ul-Huq, 2014, p.53). The flexibility element is of greater significance since the measure of adaptability of any AI assisted accounting system primarily pertains to the extent of flexibility of permutation and combinations as well as algorithmic solutions which could be generated automatically to better manage the derived data regardless of the variability of operational structures of the tasks.Wagner (2017)has determined the outcomes as the automatic recognition of the data in the most reliable and exhaustive manner without the necessity to involve any previously developed configuration. Currently, the AI based operational solutions for the accounting services have transformed the accounting service parameters which were previously restricted through older on-premise data solutions. From an academic perspective, Baldwin-Morgan (1994) has examined that most of the significant studies and methodologies which had previously dealt with the subject of impact of AI on accounting organisations, did not employ the organisational theory of Charles B. Perrow concerning the typology of technology to formulate the basis of their analysis of such impacts. Furthermore, the same scholars had also observed that most of the studies researching about the impact of artificial intelligence based Expert Systems on accounting tasks previously had only concentrated on specific case studies and had not approached the subject in a holistic manner (Issa, Sun and Vasarhelyi, 2016, p.12).

Theory of Perrow and the AI characteristics

Perrow (1970) has observed that the theoretical construct of Perrow had highlighted two particularly significant characteristics for the application of AI mechanisms such as the ES, into accounting functionalities of professionals. The initial one is the extent to which exceptions could be encountered within the specified functionalities. These exceptions indicate the total number of exceptional cases which have been encountered during any particular work such as financial calculations and estimates accounting (including the requesting of financial documents and audit plan formulation steps). Such exceptions directly impact the underlying functionalities for any accounting firm (Gordon, 2018, p.10). The second one is the magnitude and nature of the search and calculation processes which could be utilised by accounting professionals to resolve such exceptions.The exceptions generally require various particular measures of information processing which could fundamentally differ from the usual work procedures. The exceptions could be categorised through a scale of low to high (Li and Zheng, 2018). On the other hand, Perrow (1986) has opined that the searching procedures are generally reflective of the mechanisms through which any automated or manual system could be operated to detect or develop the solutions to overcome such exceptions. The emphasis of such AI mechanisms (ES and other related accounting operations management systems), is on the formulation of a spectrum of differential choices through which the most significant and accurate work procedures could be selected in an autonomous manner by the operating systems and the human involvement in such systems could be either absolutely non-existent or could be minimal at best (Kokina and Davenport, 2017, p.120). The searching process and the subsequent evaluation are all conducted on the basis of logical parameters.Baldwin-Morgan (1995)hassignified such searching as diverging from the routine tasks filed by the automated processes. The significance of AI could be thus outlined in the form of the ability of drawing upon the residue of previously unanalysed experiences of information management.

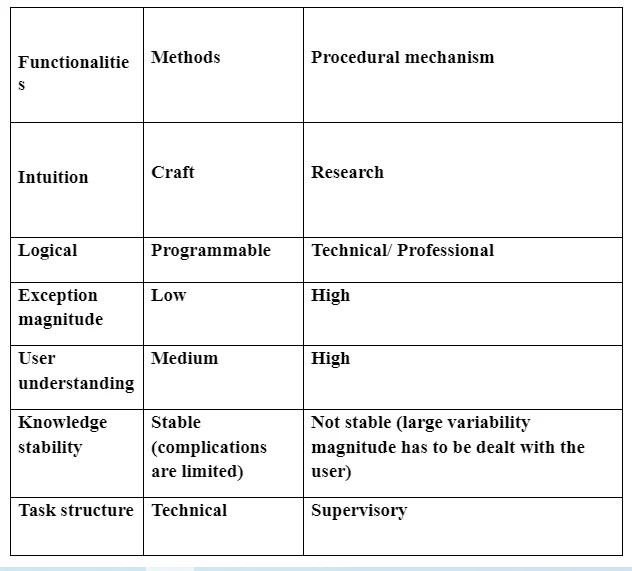

AI assisted work classification units

According to Carmichael and Willingham (1989), the two particular aforementioned dimensions could be effectively illustrated through the following table:

The above illustrated table highlights the multiplicity of descriptors for the different quadrants which are essential for accounts operations performance of the accounting professionals through the utilisation of the AI based ES applications.

AI assisted ES configuration (Technical) and effects in the accounting disciplines

Regression

This is the method which is utilised to analyse the domain knowledge derived by ES to develop an operating model which could select between two or greater number of variables (Shi, 2019, p.977). The variables are mostly continuous in their sequences and this sequence is first observed and figured out by the ES so that the suitability measure could be further determined. The involved AI algorithms are as the following:

1: Ordinary Least Squares Regression (OLSR).

2: Logistic and Linear Regression models.

3: Stepwise Regression measures.

4: Multivariate Adaptive Regression Splines (MARS).

Daft and Maclntosh (1978)have stressed on the efficacy of AI generated regression method in enabling the accounting institutions to provide the clientele organisations with the information to recover their previous remissions to the maximised extent on the basis of measuring the differential parameters of NOL (Net Operating Loss). This could be better explained in the manner that, if a company incurs extensive loss during a particular period of the financial year when the permissible deductions of the company had been greater than the incurrence of net income, then greater expenses than organisational revenue could occur during that particular period and this period of time could thus be defined as having been subjected to NOL (Omoteso, 2012, p.8492). It becomes critical for such a company to determine the exact measure of NOL so as to recover the percentage of previous payments which could be reimbursable concerning the respective nationallaws of the territories in which such a company could be registered. The combination of all of the regression algorithms of ES could effectively perform the task through retrospective calculation which could be alternatively termed as backward tracing of payables (Pannu, 2015, p.83).

Clustering algorithm utilisation

Dean, Yoon and Susman (1992)have stressed that clustering mechanism is also utilised by the different AI based accounting management approaches for the purpose of taking into account the various characteristics of existing alphanumeric data structures so as to properly define such data structures and group them into clusters through determination of representation points of each cluster of data groups.Drucker (1988)has opined that the involved algorithms are as the following:

1: Expectation Maximisation (EM). This is utilised to determine the search outcomes through logical parameters, which have been previously mentioned.

2: Hierarchical Clustering.

Dimensionality Reduction Algorithms (DRA)

This process is similar to that of clustering which detects and then utilises alphanumeric information structure which could be included within the processes data outcomes. The summarisation of data could be effectively performed through the utilisation of DRA. Duchessi and O'Keefe (1995) have outlined the involved algorithms in the following manner:

1: PCA (Principal Component Analysis) which is effective in detection of the sequential and procedural exceptions to highlight the issues in organisational financial and balance statement audit processes.

2: PCR (Principal Component Regression). This particular algorithmic application of ES, as an AI application, is utilised in cases where deferred liabilities, payments and organisational assets could become necessary to be re-accounted for after their initial direct adjustments to either the equity of shareholders or on the OCI (Other Comprehensive Income) estimates. The necessity could arise to adjust as well as accountfor the offsetting of liability effects within either the equity of shareholders or the OCI. Kelly, Ribar and Willingham (1987) have observed that particular hypothetical instances could be recognised as deferred effects involving adjustment of values of foreign currencies, evaluation of gains on unrealised holdings and calculation of losses on the available for sale securities and the estimation on cash flow hedges which could be reported as the OCI.

AI and the impact of accounting role improvement and streamlining of information utilisation

In this context, Lynch (1974) have stressed on the impact of organisational transformation which emanates from the AI application within particular work disciplines of accounting performances. This process could be further acknowledged as conversion through which the development of ES mechanisms could be finalised through utilisation of domain knowledge derived from the respective accounting organisations. Such domain knowledge could pertain to (in case of taxation) the following:

1: Calculation of the maximum and minimum measures of deduction for the Net Operating Loss (NOL) including the carryforwards which could arise at the culminations of each of the financial years.

2: Measuring the Foreign Credits (FC) in case of deductions in net earnings such as in cases where client organisations could have to remit withholding taxes which could be required to be accrued in respect to the exemptions of previously unpaid dividends (Luo, Meng and Cai, 2018, p.854). The significance of artificial intelligence assisted AI processes could be recognisable in the functions of automatically writing off the expenses of the costs of new investments which could include the depreciable assets which could have been phased out in previous cases as well. This information could be utilised in an automated manner by the ES mechanisms through the logical and programmable methods and such information could be derived for such functionalities from the domain knowledge by the AI assisted ES structures (Brynjolfsson, Rock and Syverson, 2017).

3: Combining information derived from differential sources of domain knowledge (such as respective national treasury department notices, IRS notices, proposed regulations and annual or quarterly financial bulletins which could be available on the Internet or on the organisational Intranet systems) for the purpose of effectively managing the variables such as the deductions which could be required to be made for certain organisational compensation packages (especially in case of clientele associated with construction, manufacturing, chemical, mining and nuclear technology based hazardous industries) as well as the credits and exclusions which could be necessary to be factored in to broaden the base of accurate estimate formulation.

According to March and Simon (1958), in case auditing organisational asset reports and financial performance, two significant dimensions of AI assisted ES functionalities have to be taken into consideration. These are Understandibility and Stability. In terms of accounting operations directed through the ES, the system is primarily based upon the manageability of Understandability of the domain knowledge by the automated processes along with the accounting professionals and technical support assistants who could be tasked with operating and controlling the systems. The involved ranges are effective understanding formulation to partial understanding formulation. Messier and Hansen (1987) have highlighted the dilemma of the possibility of only a handful of trained professionals or technical assistants gaining sufficient understanding regarding the input of differential variable based data in case of audit accounting within an entire department of respective accounting organisations. AI stands to change such a dilemma into a positive functionality and skill improvement prospect for any accounting firm.

Comparison between the search and exceptions

According to Michaelsen and Messier (1987), the general search processes for development of work solutions are to be expected to be controlled by the accounting professionals. This highlights the expectation of the relegation of control of ES or any other AI systems in the accounting industry to the human professionals. O'Keefe et al (1993)have noted that the outcomes of such searching process divergences are premised upon the factors of discretion entailing various alternative processes of searching. These alternative processes are mostly utilised by the auditors since they have greater responsibility of factoring in multiple sources of information such as documents and Records, examination of tangible assets, making inquiries, calculation, scanning, observation and minutes of management meetings and the associated reviews. According to Orlikowski (1992), under such conditions, the ES and other accounting AI systems are formulated as computer software which could both capture the necessary expertise from human professionals through machine learning processes and act on such information.Sviokla (1990)has termed this the heuristic operational capability enhancement process which primarily involves diagnosis of situations. AI has added this capability to the existing accounting procedures of systems diagnostics. This entails the ability to elicit expectations so as to determine the most accurate methods of dealing with such exceptions.

Comparison between Understandability and Stability

Trewin (1996)have noted that Understandability could be explained from the perspective that it directly relates to the various choices of the means through which a critical and interdependent judgement about the classification and nature of the accounting tasks could be arrived at. In this context, the ES systems generally utilise a clearly defined and delineated set of pre-programmed expertise which are periodically updated by the machine learning formats, utilised by the AI, within different accounting disciplines. Thus, through appropriate utilisation of the ES applications, the technical skill levels of accounting experts could be reinforced so as to effectively detect and resolve the information and knowledge material related errors through audits of the organisational financial performance reports. Thus, it could be understood that expectation of expertise could arise from any segment of the AI assisted audit processes of the accounting details of any client organisation and this could consistently be the points of development of ES services. As has been opined byWithey, Daft and Cooper (1983), the factor of Stability is discernable through the study of the existing number of frames and rules through which the data processing could be finalised in the auditing tasks such as verification of the assets and liabilities of the clientele through comparison of existing records and documents to the published financial statements in the format of statutory audit. The finite points of staff numbers, the value of existing assets and annual turnover amounts of client organisations have to be critically managed through such accounts auditing. Perrow (1967)has delineated that the dynamic business environments of the current era highly necessitate adjustment of consistent variations in information, data and basic technical knowledge within the accounting work processes. The measure of stability could be indicated through the extent to which such changes could be accommodated and synthesised within the automated work processes by differential AI systems such as the Expert System (ES) or the Information System (IS). According toMirzaey, Jamshidi and Hojatpour (2017), the Stability aspect is also incumbent upon the frequency at which the rules and frameworks of operations could be changing.

Interdependence between technology and supervision

The primary aspects of such an interdependence, as has been outlined byMarch and Simon (1958), has been the necessity to maintain control over the accounting functionalities.Issa, Sun and Vasarhelyi (2016)had specified that Perrow had delineated the crucial significance of coordination in between the supervisory and technical functionality units of any accounting firm for the purpose of effective execution of duties. The three characteristics of discretion, power and interdependence between various work groups of accountants have been outlined by Perrow to be the determinants on the basis of which the entire interdependence aspect between supervision and AI assisted technology could be determined. The contribution of AI in this prospect has been the ES and IS mechanisms through which greater communication could be facilitated between the individual operatives and the supervisory tiers.Kokina and Davenport (2017) have been of the opinion that business flow analysis issues could be effectively resolved through the AI facilitated technological assistance. The outcomes of AI impacts on accounting professional involvement are thus comprehensive through the incremental codification of extensive amount of knowledge and information of the existing processes of accounting in the computer programs.Li and Zheng (2018)have pointed out the greater efficacy of team based work at accounting firms has been one such impacts of AI at the accounting industry and the subsequent changes have occurred in the organisational supervisory relationships which have been facilitated by greater communication between the employees and the management levels.

Clarity of findings (research gap identified from literature)

The research gap has been identified in terms of the relative dearth of holistic understanding of the comprehensive impact of AI facilitated work processes within accounting industries.For instance, Baldwin-Morgan (1994) had concentrated their studies only on the auditing expert systems. Also, Sviokla (1990) had only examined the effect which Digital experienced after XCON was utilised and Trewin (1996) had only focused upon the impact of ExperTax automated data processing methods on the accounting firm of Coopers and Lybrand. According to Wagner (2017), these studies have only explored and evaluated individual segments of Expert Systems (ES) and not their holistic impact on the roles and contributions of accounting personnel in an extensively detailed manner. Thus, the insights provided by such studies into the impact of AI based ES mechanisms, are difficult to be generalised as well as synthesised into discernible theoretical means.

AI facilitated team work management

Team work management is impacted by the differences in the communication levels depending upon the nature and complications of the accounting services. The considerably larger complications related to accounting issues require combined efforts of different audit management teams. Such teams are primarily constituted through 11-15 auditors/accountants and such a workforce involves multiple layers of staff, seniors and managerial personnel. The team work management could thus be facilitated by AI applications through reinforcing the work roles of individual auditors/accountants by providing predictive information through which interacting activities between multiple personnel could be facilitated. This assists greatly in especially the audit process. On the other hands, the different accounting roles are mostly managed by comparatively smaller teams of professionals. This can be bettered by the AI assisted ES mechanisms through fostering real time connectivity between the upper tier management personnel and individual work units. This interconnectivity, aided by the fact that computer based AI could simultaneously manage multitasking such as storing and analysis of vast quantum of data, could enable individual accountants to be time efficient since the ES could gain critical knowledge in advance from sequential methods through which instantaneous and machine assisted decisions could be made by human operatives without having to take the time necessary to search for different strands of data (both statistical and informational).

Research methodology

The methodology utilised by the Researcher to format an effective and empirical research process concerning the evaluation of the subject under consideration could be comprehended as a combination of multiplicity of specific research tools and processes. The combination of such elements formulates the elementary foundation which supports the verifiable progress of the research data collection and analysis process. To consolidate the effort which has been so far invested in the research exercise, the Researcher has preferred to implement, as part of the overarching structure of research methodology, the research philosophy of Post Positivism, the Deductive Research Approach and the Descriptive Research Design (Newman, Benz and Ridenour, 1998). The selected research philosophy has been incumbent upon the evaluation of the disciplines of Ontology, Axiology and Epistemology.Epistemology could recognise the factual reality through the format of scrutinizing direct outcomes of interaction between different strands of human activities.Under such a method, reality is considered to be the artificial construct which emanates out of human intelligence in a subjective manner (Kumar, 2019). Thus, the element of cognitive psychology becomes significant concerning the interaction between research processes and the research participants. To consolidate the element of knowledge which could be obtained from Epistemological studies of tangible incidents/factors, the discourse of Positivism, as a research philosophical construct, could be utilised (Wiek and Lang, 2016, p.34). To consolidate the effort of accurate research data collection, the Researcher would be utilising the Post-Positivist research philosophy which has been an Epistemological evolutionary outcome of Positivism. The justification could be enunciated as the facility of empiricist observation based evaluation of research material to obtain sufficient data which, could be furnished by the Post-Positivist research philosophy, which, could, then, be quantified for the purpose of synthesising conclusions (Kothari, 2004). Furthermore, Post-Positivist research philosophy could assist the Researcher into the formulation of specific structural frameworks on the basis of which the planning of obtainment of study imperatives could become a definite possibility. The reason of this could be implied as the relatively limited measures of inappropriate interpretation of the collected research data which could be made possible under the procedural applications of Post-Positivism (Peffers et al. 2007, p.59). Authentication and verification of the collected research data would be also congruent singularities with the most extensive measures of significance which could be required for the purpose of generation of accurate research findings. Such aspects could be also effectively fulfilled through the empiricist research philosophical approach of Post-Positivism (Silverman, 2016).

The research approach

Deductive research approach accords considerable significance to the examination and testing of the theoretical or objective constructs which could be in existence for the purpose of getting utilised in any empirical research process. The emphasis is put on the effective evaluation of methodically collected data during any such researchprocess through such a research approach (Burney, 2008, p.22). This research approach is an ascending format of procedural progression in terms of application of pertinent theoretical constructs within any research project. This research approach also emphasises on the obtainment of maximised extent of research information through quantitative measures through the utilisation of comparatively large research sample sources. The Researcher has preferred to utilise the Deductive Approach on the grounds of such particular aspects which are integral to the entire practical framework of this approach. Furthermore, the synthesis of credulous, pertinent and accurate data analysis outcomes could as well be assisted by the Deductive Approach.

Research Design

Any format of research design pertains to a particularly formulated methodical framework of different techniques through which a researcher could combine multiple components of the research process through a logical and reasonable manner for the purpose of development of effective solutions to the research problems (Nassaji, 2015). The research designs are crucial in providing adequate insights of the methods through which the research process has to be conducted. Furthermore, the assessment of the research questions could be performed effectively through the selection of appropriate research designs. In this context, the Researcher would be selecting the Descriptive Research Design for the purpose of assessment of the research questions.

Justification of Research design

This research design persists to the description of the research case included within the research study in a methodical manner. The focus is on the collection, analysis and presentation of the quantitative research data through implementation of a methodical process. Thus, this research design would be effective in assisting the Researcher to obtain greater insights into the overall structure of the collected data to better delineate the developed answers for the research questions.

Selection of data collection based samples participants

The development of the test instrument was performed and then was piloted on one developer of AI systems based accounting Expert Systems as well as on one accounting institution faculty members.The test instrument was then also distributed amongst 90 other developers of the Expert Systems. These developers had been attendees of the conference on application of AI systems in different businesses including in the accounting industries. This conference had been sponsored through the American Association for Artificial Intelligence. The returns which were received had been 59 in numbers. The response rate had been 65%. The timing of the response receipt was analysed to determine any evidence of response biases and no such evidence was detected. Out of the 59 returns, exclusion of 13 responses was determined upon. The reasons had been that 2 of such respondents were not operational at that time, 8 of the respondents had pertained to research prototypes and 5 of them had not been directly associated accounting services. Furthermore, 17 other responses had highlighted that the AI based ES systems had not been properly developed. This was identified through the fact that these respondents had not managed to develop the system completely, they were unable to effectively communicate the details regarding the implementation of the respective ES mechanism in the accounting work and, in specific cases, the respondents had not been actively associated with the development of such systems.The Researcher was left with 27 effective responses which appropriately provided information on 14 different accounting functionalities and 13 financial data management. The selected research participants had been related to accounting functionalities in complete independence from those of technicians. These participants have been knowledge engineers as they had been familiar with the procedures of acquisition of information and knowledge for the operations systems of their respective accounting organisations and thus, could represent the possession of knowledge which is critical regarding work procedures which are associated with specialised computer software applications. These accounting professionals had been privy to the substantial technical expertise which is required for the purpose of constituting and maintaining the AI assisted Expert Operations Management systems. This has been the reason that these knowledge engineers had been operating in specific technical departments within their respective accounting organisations.

Research Ethics

The Researcher has taken complete sole responsibility of the ethical conducts of the entire research process. The safety and rights of the research participants have been maintained by the Researcher completely at his own accord since the rights of the research participants have been the obligations of the Researcher. Apart from this, another obligation of the Researcher has been to maintain the accuracy and integrity of the research process. The elements of confidentiality and personal information of the questionnaire respondents have been maintained by the Researcher under consideration so that the rights of the participants could be safeguarded. Finally, the obtainment of prior consent from the selected research participants has been central to the ethical considerations performed by the Researcher of the associated research study.

Relevance and understanding shown in data analysis methods

The corresponding section has summarised the data analytical findings and research revelations. The reviewing of the overall results regarding the utilisation of the ES in the accounting processes has been undertaken. The comparative specifications between the existing ES services have been also analysed. Furthermore, the data has been effectively summarised through the application of a tabular format.

Aggregate result evaluation

The evaluation of the aggregate outcomes could indicate the fact that expert systems could be efficient in permitting the accountants to exercise extensive control on the search solution as well as greater discretion is available to the user regarding implementation of the recommendations of the systems. Consequential discretion is also available to the users of the ES mechanisms to decline greater supervision control and to access the top management with greater frequency. Problems with greater complications and broader range could be solved through the AI systems and this could permit greater span of multitasking on part of the accountants/professionals. Effective evaluation of the accountingroles and operations of accounting professionals could indicate that audit mechanisms could garner better control over the search processes. Lesser supervision and greater autonomy are associated with AI systemswith greater range of decisions availability. Furthermore, it was observed that even though the AI assisted systems areintegral to the accounting disciplines, there could be a number of different noticeable divergences amongst the functionalities associated with the two. Analysis of the statistical results has been assisted through the means which have been generated in five of the questions and these have been indicative of the differences between the two work processes.

Limitations of the research

The primary research limitation has been the dearth of time which has constricted the Researcher from including greater number of research participants within the entire research study process. The time deficiency factor has also barred the Researcher from undertaking of serious pilot testing of the concept propounded by Perrow. The purpose of the research undertaking had been to determine the impact of AI on the functionalities of the accounting professionals through application of empirical evidence and to highlight the subsequent implications on the accounting organisational functionalities as well. Thus, the Researcher had intended to include the factors such as influence on the supervisory format, the facilitation of accessibility to the top management and the decision ranges involving the organisational issues which could be observed. However, the final selection of only 27 different participants has compelled the Researcher to only concentrate on the singular domain of accounting work based implications. As a direct outcome of the limited research participant base, the differential accounting activity based implications of AI on the accounting professionals have not been properly determined. Furthermore, the limited research participant base has been also the reason that the Researcher has utilised the general technology based approach in determining the data findings as opposed to the AI applications which could be analysed as definite tools for the accounting professionals for work performance management.

Conclusion

The preceding research study has been focused on the evaluation of the impact AI assisted technical support mechanism (Expert Systems) has on the work discipline of accounting. The impacts of Expert Systems have been particularly significant concerning the differential extents to which individual operations pertaining to the two specific categories of accounting could be influenced. In this context, the comparative results of the impacts of ES on operational management of respective roles and responsibilities of the accounting professionals had been evaluated and summarised with the assistance of the theoretical framework of Perrow. Such average results were utilised to place the data regarding these two systems in the tabular format. The range which was provided within the test instrument had been utilised to provide adequate placement of the research outcomes based on an assertive interpolation.

Reference List

Appelbaum, D., Kogan, A., Vasarhelyi, M. and Yan, Z., 2017.Impact of business analytics and enterprise systems on managerial accounting.International Journal of Accounting Information Systems, 25, pp.29-44.

Baldwin-Morgan, A.1994. The impact of an expert system for audit planning: Evidence from a case study, International Journal of Applied Expert Systems. 2(3), 159-174.

Baldwin-Morgan, A.1995. Studies of the impact of accounting-related expert systems: Comparison of methods, IEEE Conference on Artificial h~telligence Applications, IEEE Press, Washington, D.C., 72-77.

Brynjolfsson, E., Rock, D. and Syverson, C., 2017. Artificial intelligence and the modern productivity paradox: A clash of expectations and statistics (No. w24001). National Bureau of Economic Research.

Daft, R., and Maclntosh, N.1978. A new approach to the design and use of management information, California Management Review. XXI: 1, 82-92.

Dean, J., Yoon, S., and Susman, G.1992.Advanced manufacturing technology and organisation structure, Organisational Science.3(2).

Duchessi, P. and O'Keefe R.M. 1995.Understanding expert system success and failure, Expert Systems With Applications. 9(2), 123-133.

Gordon, L.A., 2018. The Impact of Technology on Contemporary Accounting: An ABCD Perspective. Transactions on Machine Learning and Artificial Intelligence, 6(5), pp.10-10.

Guo, X., 2019, November.Research on the Transition from Financial Accounting to Management Accounting under the Background of Artificial Intelligence. In Journal of Physics: Conference Series (Vol. 1345, No. 4, p. 042031). IOP Publishing.

Issa, H., Sun, T. and Vasarhelyi, M.A., 2016. Research ideas for artificial intelligence in auditing: The formalization of audit and workforce supplementation. Journal of Emerging Technologies in Accounting, 13(2), pp.1-20.

Kelly, K., Ribar, G., and Willingham, J. 1987. Interim report on the development of an expert system for the auditor's loan loss evaluation, Proceedings of the ToucheRoss~University of Kansas Audit Symposium.167-188.

Kokina, J. and Davenport, T.H., 2017. The emergence of artificial intelligence: How automation is changing auditing. Journal of Emerging Technologies in Accounting, 14(1), pp.115-122.

Li, Z. and Zheng, L., 2018, September.The Impact of Artificial Intelligence on Accounting.In 2018 4th International Conference on Social Science and Higher Education (ICSSHE 2018).Atlantis Press.

Luo, J., Meng, Q. and Cai, Y., 2018. Analysis of the Impact of Artificial Intelligence application on the Development of Accounting Industry. Open Journal of Business and Management, 6(4), pp.850-856.

Marshall, T.E. and Lambert, S.L., 2018. Cloud-based intelligent accounting applications: accounting task automation using IBM watson cognitive computing. Journal of Emerging Technologies in Accounting, 15(1), pp.199-215.

Messier, W. and Hansen, J. 1987. Expert systems in auditing: The state of the art, Auditing: A Journal of Theory and Practice. 7(1), 94-105.

Mirzaey, M., Jamshidi, M.B. and Hojatpour, Y., 2017.Applications of artificial neural networks in information system of management accounting.International Journal of Mechatronics, Electrical and Computer Technology, 7, pp.3523-3530.

Moudud-Ul-Huq, S., 2014. The Role of Artificial Intelligence in the Development of Accounting Systems: A Review. IUP Journal of Accounting Research & Audit Practices, 13(2).

O'Keefe, R., O'Leary, D., Rebne, D., and Chung, Q.1993. The impact of expert systems in accounting: System characteristics, productivity and work unit effects, International Journal oflntelligent Systems in Accounting, Finance and Management. 2(3), 177-189.

Orlikowski, W.1992. The duality of technology: Rethinking the concept of technology in organisations, Organisational Science. 3(3).Perrow, C.(1967) A framework for the comparative analysis of organisations, American Sociological Review. 194-208.

Peffers, K., Tuunanen, T., Rothenberger, M.A. and Chatterjee, S., 2007. A design science research methodology for information systems research. Journal of management information systems, 24(3), pp.45-77.

Peffers, K., Tuunanen, T., Rothenberger, M.A. and Chatterjee, S., 2007. A design science research methodology for information systems research. Journal of management information systems, 24(3), pp.45-77.

Shi, Y., 2019, February. The Impact of Artificial Intelligence on the Accounting Industry.InThe International Conference on Cyber Security Intelligence and Analytics (pp. 971-978).Springer, Cham.

Skilton, M. and Hovsepian, F., 2017. The 4th Industrial Revolution: Responding to the Impact of Artificial Intelligence on Business. Springer.

Trewin, J. 1996.The impact of an expert system on a professional accounting organisation, International Journal of hztelligent Systems in Accounting, Finance and Management. 5(3), 185-197.

Wagner, W.P., 2017. Trends in expert system development: A longitudinal content analysis of over thirty years of expert system case studies. Expert systems with applications, 76, pp.85-96.

Withey, M., Daft, R., and Cooper, W.1983. Measures of Perrow's work unit technology: An empirical assessment of a new scale, Academy of Management Journal, 1983.26(1), 45-63.

- 24/7 Customer Support

- 100% Customer Satisfaction

- No Privacy Violation

- Quick Services

- Subject Experts